Introduction

Directors, being the principal officers of the company, need to act honestly to discharge the duties entrusted to them in good faith and at all times for the best interest of the company. This is clearly provided in s 213 of the Companies Act 2016 (CA 2016).

In the event of a default, these directors would be jointly and severally liable for any misconduct in depriving the company from making the needed profit or are accountable for any profit which is unjustly enriched by them for their own benefits.

In order to assess damages, the court would be assisted by expert evidence in arriving at a just and fair quantum. Expert evidence would also be concurrently relied on by the directors to mitigate their liability.

In short, expert evidence would be presented by both parties to substantiate the claims advanced by the litigant, as well as the other parties, i.e. the directors in mitigating the damages.

Expert evidence

Experts are professionals having the essential core technical skills, equipped with adequate experiences in their respective fields and are commonly accepted in their own profession as being experts or leading experts. The object of expert evidence in every case is solely to provide independent assistance, guiding the honourable court to make an informed decision. Expert evidence is never conclusive; after all it is merely opinion evidence which can never be equivalent to substantive evidence.

It is a trite law that the court is the final decision maker on any expert evidence. It would decide to accept or reject the admission of any expert evidence which would be given appropriate weightage and credit to its relevancy, applying to the factual matrix of the case.

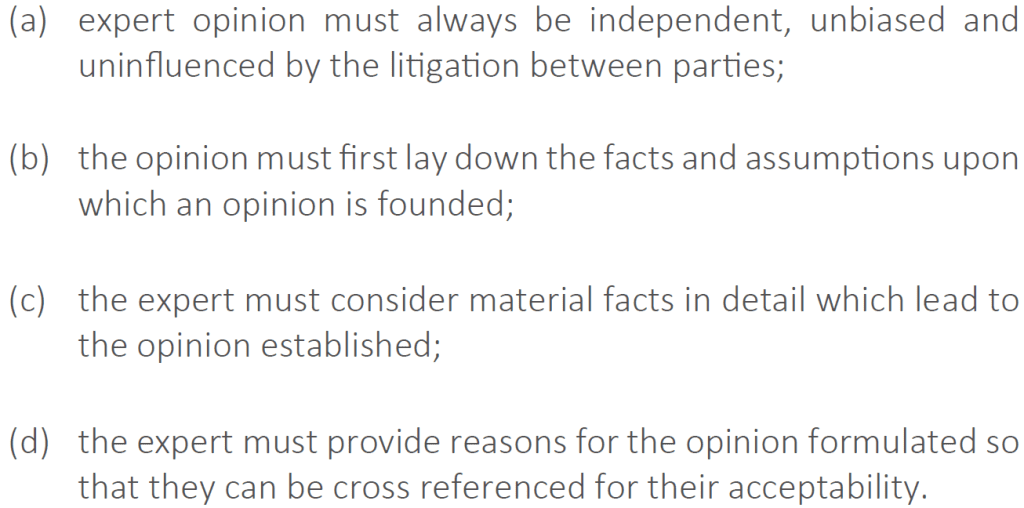

The expert evidence needs to adhere to the following golden thread rules to frame up an unequivocal opinion:

In the upshot, the court would review the expert evidence with caution, assess and evaluate the reason for the opinion and take into account other relevant evidence and then make a decision whether to accept, modify or to reject it in its totality. The character of the expert and his demeanour in the court would also play a significant role in the court’s decision to accept or to reject such expert evidence.

Practical illustration

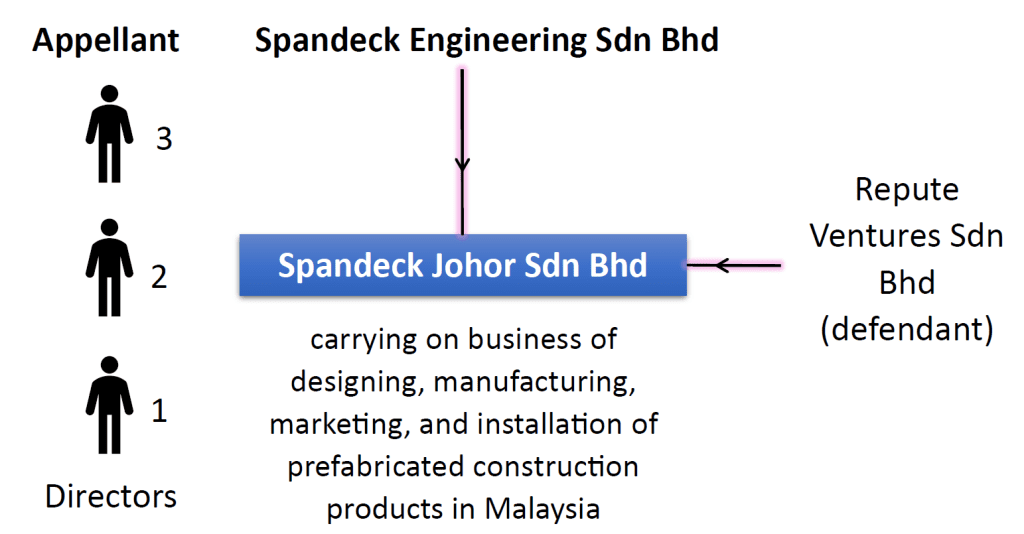

In Chi Chao-Ton Tony & 2 Ors v Repute Ventures Sdn Bhd [2019] 1 AMR 841, the appellant were the directors of the company, Spandeck Johor Sdn Bhd, whose 51% was owned by Spandeck Engineering Sdn Bhd (the majority shareholder). On their own accord, they had removed four (4) items of machines for safekeeping purposes, in view of the factory site not being ready.

Due to the failure to obtain the necessary licenses and business permits to conduct its pre-cast business, the factory was eventually never constructed and the said company had never started any businesses or operations. These machines had, in fact, never been used.

The defendant, Repute Ventures Sdn Bhd, which was the minority shareholder of 49% then proceeded with the winding up order and applied to the court for compensation under the then s 305 of CA 1965 (now s 541 of CA 2016) against the appellants on the grounds that the appellants had failed to return the machineries to the liquidator for the completion of the winding up process.

The High Court was asked to assess the damages to be paid taking into account:

(a) the deprecation of the machine; and

(b) the depreciation rate of the machine,

based on acceptable accounting standards.

The crux of the issues

The machineries were purchased on 10.8.1998 and were removed on 28.1.1999 for safe keeping. The minority shareholder (Repute Ventures Sdn Bhd) commenced legal action on 27.3.2007 to wind up the company. On 8.1.2008 (after approximately 10 years), the company was wound up on just and equitable grounds.

It is a finding of facts that the directors had indeed failed in their duties to provide the company with statements of affairs to facilitate the winding up process, it had also defaulted in returning the four (4) earlier removed machines to the liquidator.

In his audit report regarding the damages to the company, PW1 unequivocally stated that based on accepted standard accounting principles, there was no depreciation of the machineries as they were never utilized for production at all by the company.

The High Court, after taking up the expert evidence of PW1, an accountant and auditor with an experience of 30 years, held that compensation for the value of the machineries at the date of the winding up order would be the sum equal to the initial purchase price in 1998.

On 17.6.2011, the High Court ordered that the directors to be personally and jointly liable to the value of the four (4) machineries based on their original price. The directors were to compensate Spandeck Johor Sdn Bhd the sum of RM1,795,531.45 being the purchase price of the machineries in 1998.

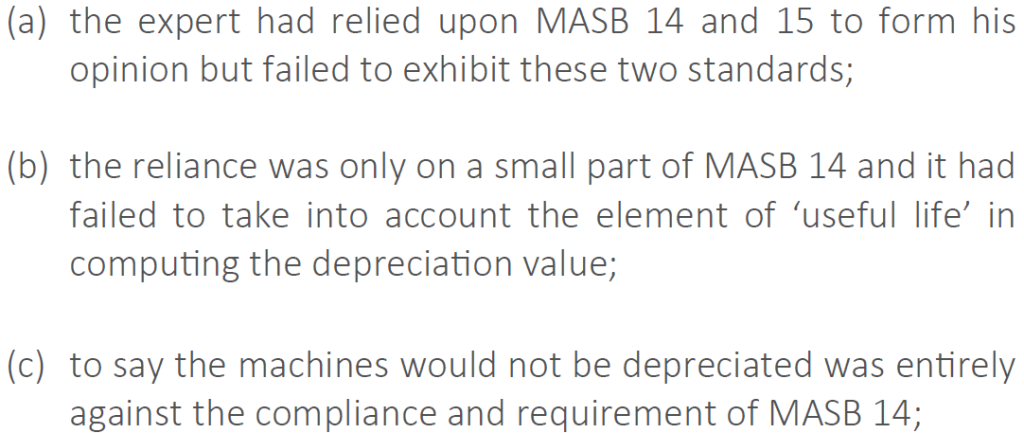

Being dissatisfied, the appellants appealed to the Court of Appeal. The learned counsel for the appellants submitted that the learned judge had erred in wholly relying on the auditor’s report. The learned counsel contended that the auditor’s report should not have been relied upon by the learned JC as PW1 had failed to exhibit Malaysian Accounting Standard Board (MASB) 14 and MASB 15, or the whole MASB which formed the basis of the auditor’s report or opinion.

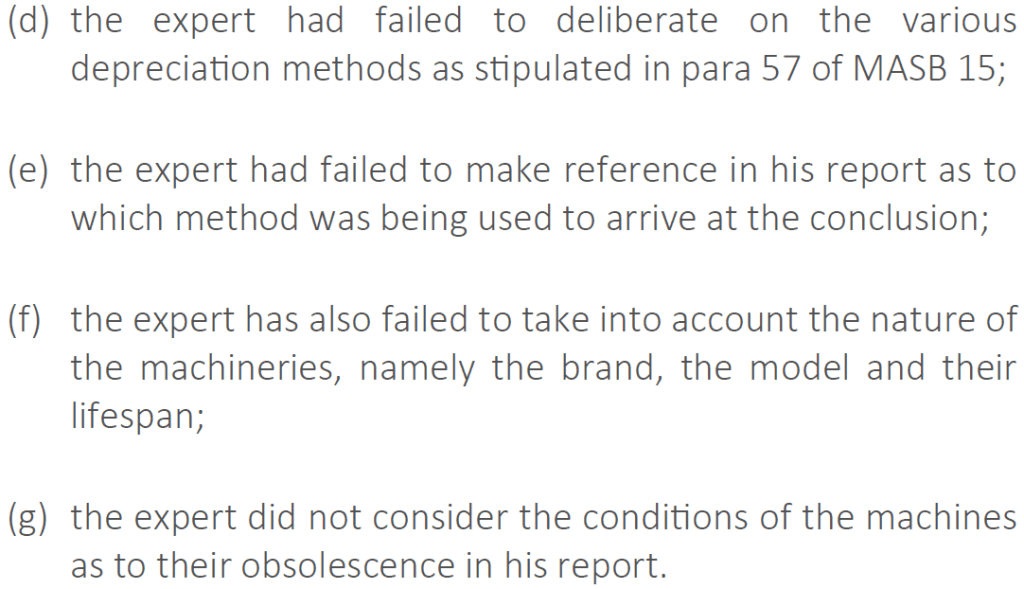

The Court of Appeal then concurred and found that the expert evidence (PW1) was unreliable and not satisfactory due to the following shortcomings or defects:

These four (4) machines were purchased on 10.8.1998 and were removed and properly stored for safekeeping following the decision made in the management meeting held on 28.1.1999. The appellants had advanced an argument that, based on a minimum of 10% yearly depreciation, the machines would have zero value after 10 years. This would mean that the directors do not need to account for the damages.

The Court of Appeal found that this argument of zero value was totally irrelevant and not acceptable in its entirety. The facts revealed that the four (4) machines were taken out within a year and had never been used, and therefore the true construction would mean the depreciation of 10% of the purchase value was to be awarded. The directors were still required to account for the 90% value to the company.

Conclusion

The enactment of the new Companies Act 2016 imposes onerous responsibilities on the directors. In the Federal Court’s decision of Dr Shanmuganathan v Periasamy s/o Sithambaram Pillai [1997] 3 MLJ 61, Anuar CJ reiterates the trite law that the principal object of an expert evidence is to assist the court to form its own opinion. The opinion must be accompanied by the reasons.

The shareholders would rely on the expert assistance to frame their claim, so would the directors who must equally be supported by their own expert(s) to refute or mitigate their liability. The careful selection of expert matters most of all.

*Dr. Choong Kwai Fatt is a practicing advocate & solicitor of the High Court of Malaya.

Note: The deliberation on “Expert Evidence – The Mitigation Factors on Directors’ Risk” is the writer’s own opinion and conclusion.

References:

- Hallmark Legal Principles on Companies Act 2016, Choong Consultants Plt, 2019, 1st ed.

- Dr Choong on Companies Act 2016, Peng You Solutions Plt, 2020, 3rd ed. (email at pengyou.solutions@gmail.com)

- Dr Choong on Interpretation of Companies Act 2016, Peng You Solutions Plt, 2020, 1st ed.

- Single Person Company, InfoWorld, 2018, 2nd ed.

- Practical Guide on CLP Evidence, Peng You Solutions Plt, 2019, 1st ed.

- Practical Guide on CLP Civil Procedure, Peng You Solutions Plt, 2019, 1st ed.